Conventional MMM is short-term focused

The conventional Marketing Mix Model (MMM) deals predominantly with short-term marketing effectiveness, where dynamic specification in the form of Adstocks focuses on ‘mean reverting’ or transitory effects over several weeks or months. However, long-term effects, reflecting the persistent changes in core brand preferences inherent in genuine brand-building behaviour, are often ignored.

A popular remedy

A conventional solution is the use of Brand Equity metrics, where the mix model is augmented with survey-based ‘mindset’ metrics such as unaided brand awareness or brand consideration, together with sub-models for the chosen metric in terms of advertising variables. The indirect effects of advertising on sales are then interpreted as long-term effects.

Drawbacks

However, simply adding brand metrics directly to the standard MMM equation is an ad hoc and internally inconsistent way of measuring brand equity effects for three main reasons.

Ignores the fundamentals of time series econometrics

If (observable) brand building effects exist, then sales need to exhibit evolutionary/trending behaviour.

- If sales are not evolving, then any regression of brand metrics on sales can only be a short-term relationship by definition. It doesn’t matter if the brand metric is ‘defined’ as a long-term construct. Any indirect marketing effects on the brand metric through to sales are necessarily short term.

- If sales are evolving, we cannot just run simple regressions of sales on marketing and brand metrics. If marketing and brand metrics are stationary, then the mix equation is unbalanced and we must first-difference sales. If brand metrics are also evolving, then there is potential for spurious regression problems. Brand equity metrics must also be first-differenced and valid cointegrating (non-spurious) relationships between sales and brand metrics need to be incorporated.

Alleged long-term constructs are regressed directly on sales

- A plausible theory of brand-building would link the long-term brand preferences embodied in mindset metrics directly to the long-term purchase demand revealed through base sales. This follows naturally from the fact that base sales and attitudinal data both represent brand health and are essentially two sides of the same coin.

- The use of total sales is, therefore, ad hoc and obscures long-term movements, risking contamination with short-term transactional effects

Does not adequately reflect the brand-building process

- Simply adding brand metrics as an additional regressor precludes feedback between (base) sales, earned media and other long-term drivers

- Feedback effects mimic word-of-mouth effects as consumers talk about brand experience leading to new trialists and growth of the loyal customer base

- Only by identifying these endogenous relationships in a suitable network model structure such as a Vector Autoregression (VAR) can we estimate the true incremental long-term impact of marketing on base sales via brand perceptions

Ignoring these issues leads to misestimation of the (base) sales impact of brand metrics and thus misleading inference on long-term (indirect) media effects. To see why this happens, we demonstrate the issues involved in a worked example using our BaseDynamics approach.

Worked example

Step 1: Unobserved Component Model (UCM) of sales

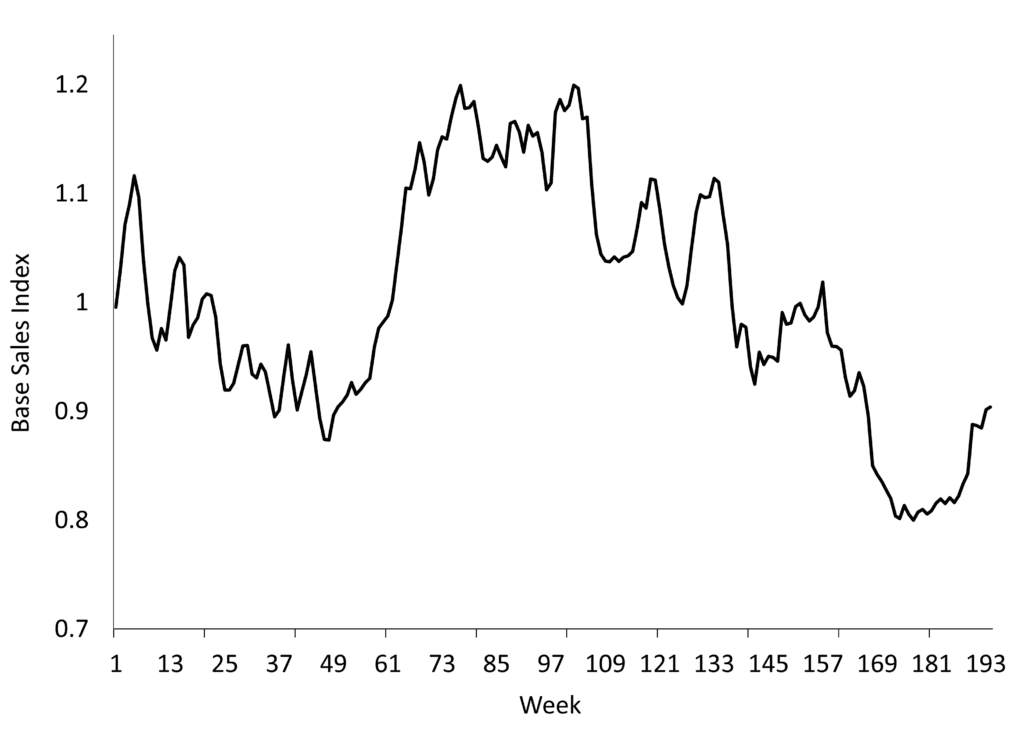

We start with a UCM model of daily sales, controlling for all short-term marketing effects. We then extract the dynamic (long-term) base line and aggregate to the weekly frequency as illustrated in Figure 1.

Figure 1: long-term base sales

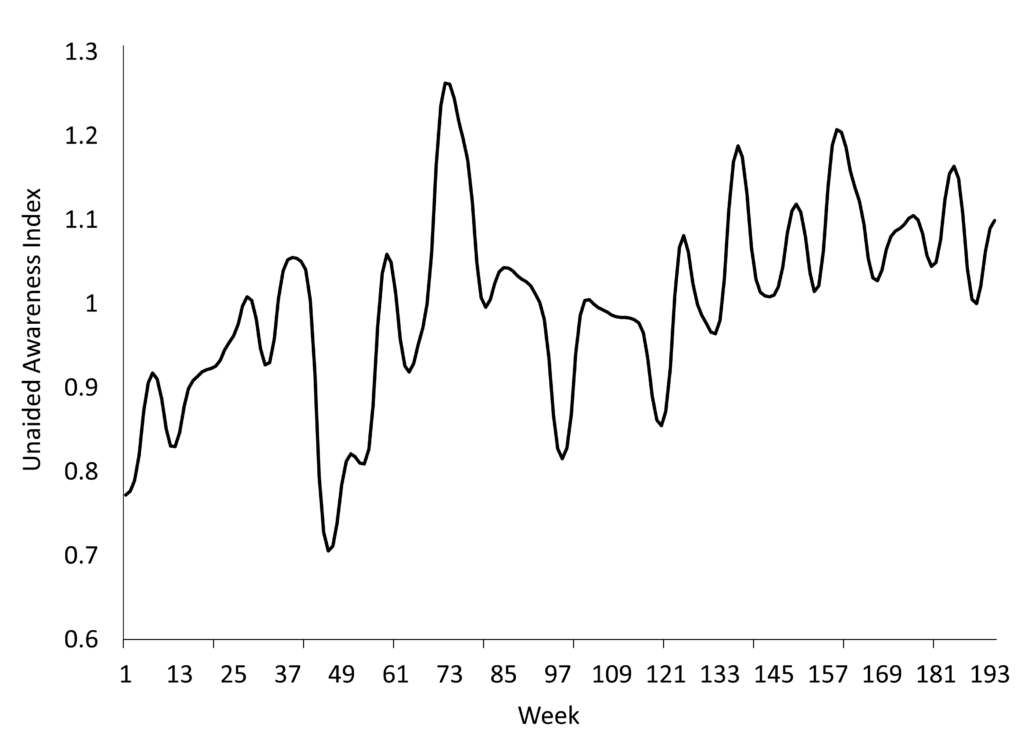

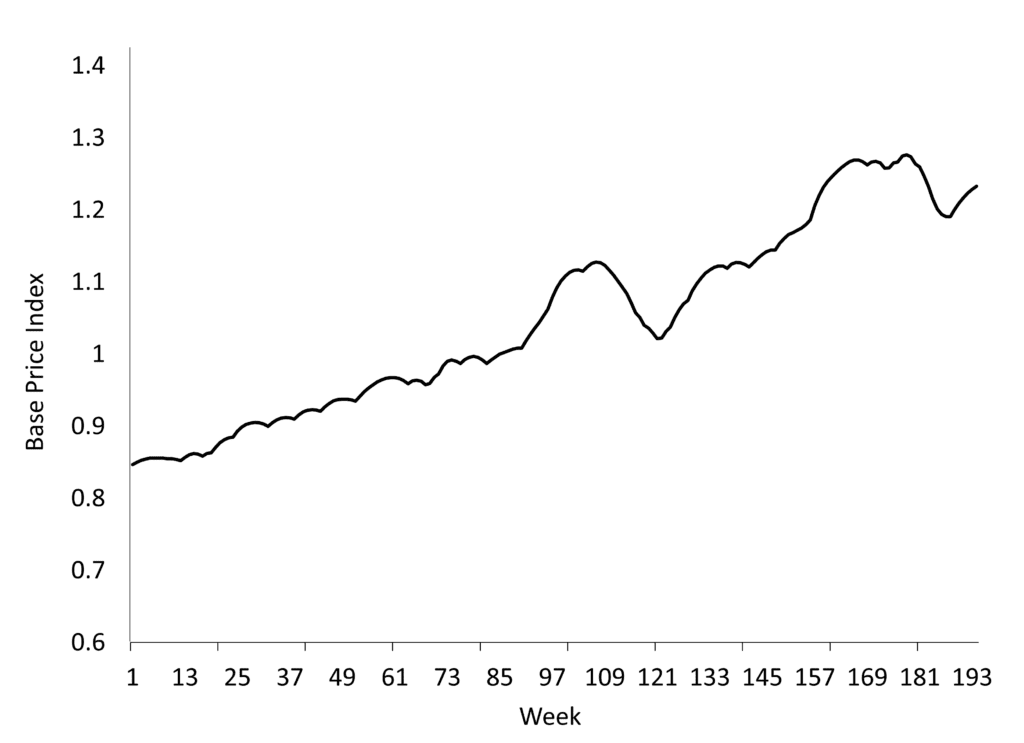

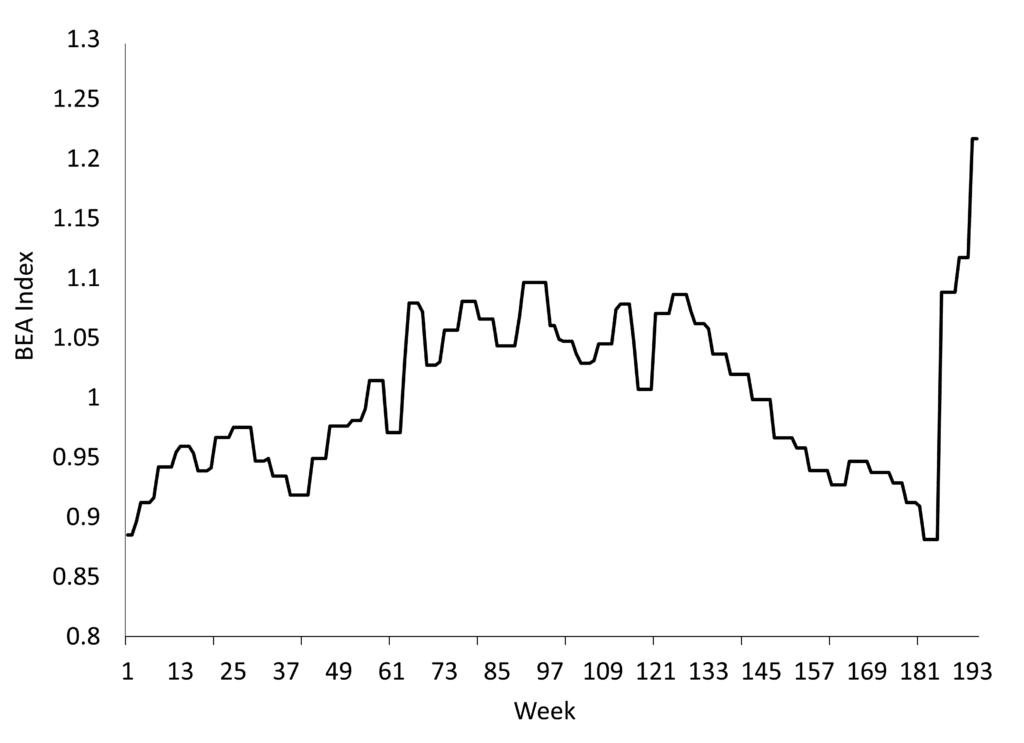

Standard ADF Testing showed that base sales is an evolving (non-stationary) process, potentially indicative of persistent brand-building behaviour. In order to test for and quantify such effects, we collected data on consumer brand perceptions (unaided brand awareness) together with base price and business economic activity (BEA) to control for other sources of long-term growth. All data are illustrated in Figure 2:

Figure 2: brand perceptions and trend controls

Unaided Awareness Base Price Business Economic Activity

Step 2: A Vector Error Correction Model of base sales

To quantify the dynamic relationships between base sales, brand perceptions and controls, we estimate an unrestricted VAR, including data on paid and earned media. The VAR(1) form is set out in Figure 3, where Advt represents paid TV GRPs and zt represents earned media metrics such as social media and product reviews. Both are stationary and exogenous in this example but need not be so.

Figure 3: unrestricted VAR form

$Base_t = \alpha_{11}Base_{t-1} + \alpha_{12}Aware_{t-1} + \alpha_{13}Price_{t-1} + \alpha_{14}BEA_{t-1} + \beta_1Adv_t + \delta_1z_t + \epsilon_{1t}$

$Aware_t = \alpha_{21}Base_{t-1} + \alpha_{22}Aware_{t-1} + \alpha_{23}Price_{t-1} + \alpha_{24}BEA_{t-1} + \beta_2Adv_t + \delta_2z_t + \epsilon_{2t}$

$Price_t = \alpha_{31}Base_{t-1} + \alpha_{32}Aware_{t-1} + \alpha_{33}Price_{t-1} + \alpha_{34}BEA_{t-1} + \beta_3Adv_t + \delta_3z_t + \epsilon_{3t}$

$BEA_t = \alpha_{41}Base_{t-1} + \alpha_{42}Aware_{t-1} + \alpha_{43}Price_{t-1} + \alpha_{44}BEA_{t-1} + \beta_4Adv_t + \delta_4z_t + \epsilon_{4t}$

On face value Figure 3 mimics the standard type of ‘nested’ sub-equation approach where, for example, paid and earned media impact a sales outcome indirectly through awareness. However, BaseDynamics goes well beyond simply adding brand perception data as an additional regressor to a short-term mix model. It represents a full dynamic system, allowing feedback between base sales, brand perceptions, price and economic activity to explain the mechanics of brand-building and long-term growth.

To add some economic structure, we then test for and impose any long-term cointegrating (equilibrium) relationships between base sales, unaided awareness, BEA and price to create a Vector Error Correction Model (VECM). If mindset metrics are to provide a credible statistical and economic foundation for brand-building, we would expect unaided awareness to share a common trend with (base) sales. We find one such relationship. The estimated cointegrating relationship (CV), error correction (alpha) coefficients and full long-term (impulse response) coefficients are illustrated in Table 1.

Table 1: VECM model outputs

Cointegrating Relationship

| Regressor | CV | Alpha |

| Base sales | 1 | -0.151 (-3.8) |

| Base Price | -0.588 (5.10) | 0 |

| Awareness | 0.280 (2.10) | 0.082 (2.10) |

| BEA | 1.81 (4.90) | 0.060 (3.70) |

Impulse Response Coefficients

| Equation | $\sum\varepsilon_{Base}$ | $\sum\varepsilon_{Price}$ | $\sum\varepsilon_{Aware}$ | $\sum\varepsilon_{BEA}$ |

| Base sales | 0.455 (6.40) | -0.688 (-3.60) | 0.130 (2.70) | 0.960 (4.00) |

| Base Price | -0.005 (-0.01) | 1.370 (10.00) | 0.006 (0.20) | -0.020 (-0.10) |

| Awareness | 0.196 (1.80) | 0.080 (0.30) | 0.889 (12.50) | -0.721 (-1.21) |

| BEA | 0.221 (5.70) | 0.054 (0.05) | -0.063 (-1.10) | 0.639 (4.90) |

- The cointegrating coefficient between unaided awareness and base sales in the left-hand panel is 0.28.

-

- This captures the underlying equilibrium (attractor) relationship between base sales and unaided awareness and embodies feedback reflected in the alpha parameter of 0.085.

- The impulse response coefficient for unaided awareness in the top row of the right-hand-side panel is 0.13.

-

- This captures the final long-term impact of unaided awareness on base sales conditional on all short and long-term dynamic interactions and exogenous regressors.

Conclusion

The conventional approach ignores all such effects. This leads to mis-estimation of the long-term impact of brand equity metric(s) on sales, the dynamics of brand-building and, by extension, long-term media impacts.

To read more on these issues, see our latest publication on modelling long-term effects in the marketing mix.

Talk to us about measuring the full impact of brand-building on sustained sales growth.